-

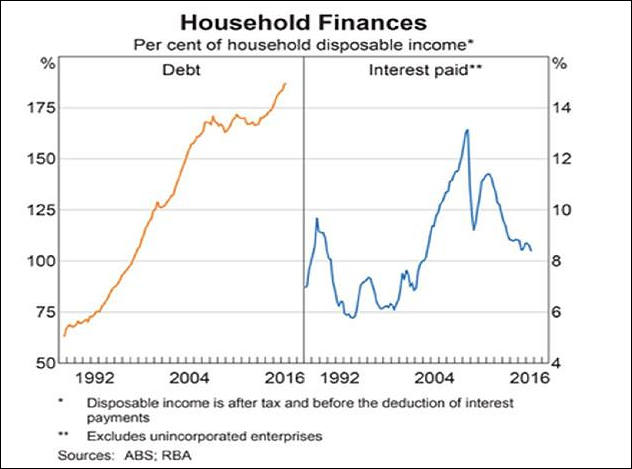

Australian Household Debt

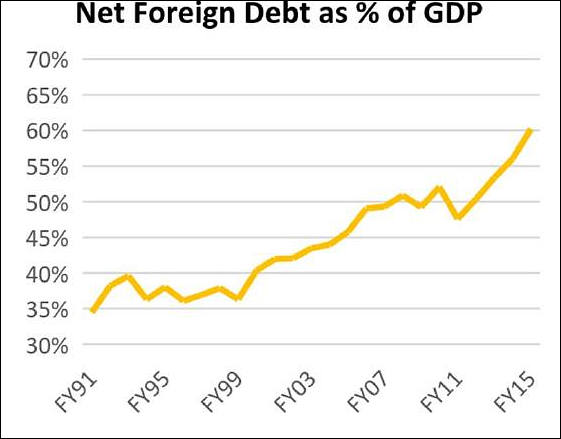

Net Foreign Debt

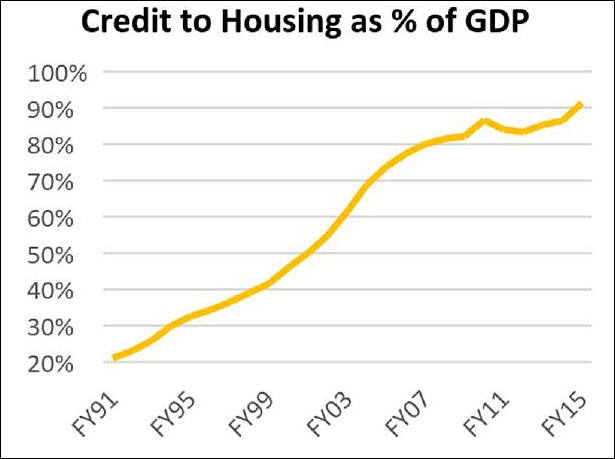

Housing Bubble

-

Cost of housing in Melbourne and Sydney is about equal 4th in the world, and intersest rates are still at lowest ever now. I think that's reflected in the first graph, or maybe it's showing that only repayments on principal are being paid? Auction clearances are still at all time high, and housing price boom still happening because of developers and baby boomers puffing the price. Young people getting into market want brand new house, new furniture, new car, and still travel the world...all on credit. Goverment spent our huge surplus after GFC (2008) on stupid initiatives to avoid slow down. Our mining boom is over, no local industries any more, and interest rates WILL go up. When interest rates go up employment could take a whack, housing prices will fall, young people will still have 90-95% debt in their property...the rest will be history repeating itself. I haven't mentioned business and the consequence of interest rises because it's a all a bit too academic (economics) for me to coment, but a lot of young people and young business people have never experienced high interest rates in their adult life. I'm holding on tight.

-

I live in Switzerland and I plan to move to Australia to live there. I went there 4 times but last time was more than 15 years ago! We just had our 2nd child so we'll wait a couple of years before moving out. I hope that I'll find work easily in Sydney, I am a motion designer and videographer. Any advice Haderdasher?

-

Hi @tenjin, I have worked mainly in the television industry as a freelancer, AD, floor manager, assistant producer etc, in Melbourne. So my advice on work would come from that angle. But I’d rather stay on topic with the Australian economy, and advice concerning moving over here with wife and 2 children. It’s good that you are thinking about doing it in a couple of years because I firmly believe the good times here in Australia are historically going to go the same as all of our booms in the past. The cost of housing is reaching the point of madness, and the great Australian dream has always been home ownership, and young people have been borrowing insane amounts of money to compete against developers, people of my age buying 2nd properties as superannuation schemes with tax concessions, and their own demographic to get into the market. When interest rates start going up, as they will soon, a lot of people are going to be caught out with very little collateral in their house, and their property will be worth far less than what they purchased it for, so the Banks will move in and we’ll see fire sales all over the place because they can’t make repayments. You really need about $1.3-1.5 million AUS at the moment to buy with in 30k of Sydney or Melbourne, or else you’ll be travelling 4-5 hours a day to and fro from work, and living in the sticks. To work in your field you need to be pretty close to town. I haven’t been to Switzerland for 40 years, but stayed with a family in Dotzigen for a while and although they had a good standard of living, they were wise with their money and hard workers. So maybe you should evaluate your current worth and make a comparison as to how much it would cost to sell up and buy up in Oz on today’s market. As far as employment goes feel free to message me and I’ll be able to give advice on the freelance market here, but mainly concerning camera work as I work with quite a few good DOP’s. But in essence I think this is how it’s going to happen here in Australia very soon, “we will go to bed on a Saturday night after another day of record auction prices and clearances, and wake up on Sunday to news that the reserve bank is increasing the 1st of several rate increases”, and by Monday night’s News programme panic will have hit the market. Hope I haven't scared you off, but that's the way I'm seeing it at the moment and I hope I'm wrong. Cheers mate.

-

Reserve Bank of Australia governor can't change goverment policy, but he can control the interest rate on loans. Personally I think he will do more than just hold interest rates at current levels.

http://www.abc.net.au/news/2017-02-24/philip-lowe-house-committee-economics/8299714

In 1992-4 I was paying 18% interest on my mortgage and doing it hard, but because of the cost of a house on today's market I think I had it easier. So lower interest rates aren't the complete answer to housing affordability. The housing boom has been like rivers of gold to the state goverments with stamp duty on the purchase of a property, not to mention a money making tool for local councils, and government departments, when it comes to conveyancing disbursements costs. The important people in all of this are the young families, and the goverments just sucks every last penny out of them

-

I think current homes prices reflect first stages of marginal collapse. Big amount of people who are middleman and such are forced to increase prices on things you can not live without to keep average margins on level where system can sustain itself.

-

@Vitaliy_Kiselev Agreed, and I would add Government to list of middleman. Like I said housing boom has been rivers of gold for them. Infact it is keeping my state goverment in the black.

-

AFAIK nobody at the Reserve Bank has mooted an interest rate rise any time soon. OTOH their new Governor has come out and pointed to ending the elephant in the room, "Negative Gearing" as being the only way house prices can slow "for a while. " (Negative gearing law allows people who buy an investment home to claim their loan interest as a tax deduction).

With the possible end of Negative Gearing, the end or slowing of Australia's housing bubble will not need any interest rise to get ordinary home owners into trouble : as soon as your house is worth less than your mortgage you can default and banks will foreclose - the same as in the States.

-

I think interest rates will be heading North by the end of the year, and Philip Lowe is on the front foot with it all. He's all but come out and said "the party is over with any further cuts" Negative gearing seems to be only part of the problem if those articles I linked are correct.

-

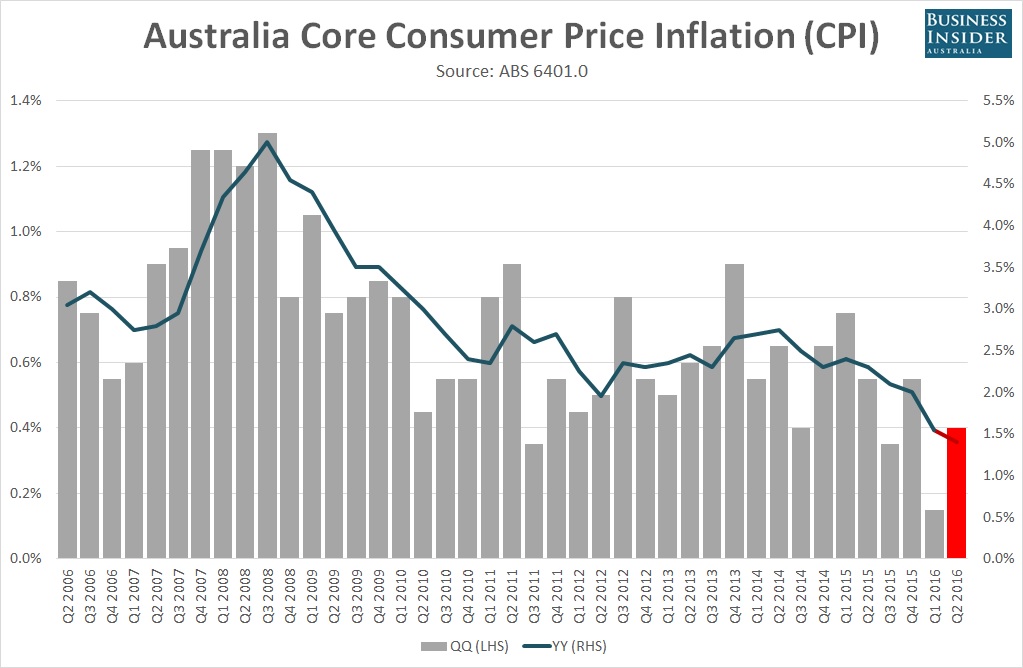

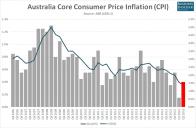

from Business Insider Australia http://www.businessinsider.com.au/heres-what-economists-are-saying-before-this-weeks-crucial-australian-inflation-report-2016-7

tmp_13962-Core-Australian-inflation-rate-preview-q2-20161282369683.jpg1023 x 668 - 136K

tmp_13962-Core-Australian-inflation-rate-preview-q2-20161282369683.jpg1023 x 668 - 136K -

There are two emerging classes in Australia: those who own their homes (and sometimes own investment homes) and those who'll never own their homes - and try to find affordable rental housing.

Quite naturally, those who cannot come up with the rent are starting to spill onto city streets, much to the embarrassment of the well-heeled shoppers.

Police move in on homeless people and supporters at Melbourne camp

-

You sound like someone who can be confident of entry to Australia, so you may well find employment in your media field.

For others intending to emigrate to Australia, it's a good idea to look up our immigration points system for different kinds of visitors. (Basically the country selects people we need - so the healthy, honest, English-speaking, solvent and trained tend to get chosen).

Unless people qualify for immigration under family reunion or political asylum grounds, (which awards them high points) the bulk of candidates fall into the employment based category as specified on the Department's website: https://www.border.gov.au/Trav/Work/Work/Skills-assessment-and-assessing-authorities/skilled-occupations-lists/CSOL

Film and TV graduates do figure on the list (notably, video producers aren't needed much according to a note I read somewhere on the website):

- Artistic Director 212111 VETASSESS

- Media Producer (excluding Video) 212112 VETASSESS

- Radio Presenter 212113 VETASSESS

- Television Presenter 212114 VETASSESS

- Author 212211 VETASSESS

- Book or Script Editor 212212 VETASSESS

- Art Director (Film, Television or Stage) 212311 VETASSESS

- Director (Film, Television, Radio or Stage) 212312 VETASSESS

- Director of Photography 212313 VETASSESS

- Film and Video Editor 212314 VETASSESS

- Program Director (Television or Radio) 212315 VETASSESS

- Stage Manager 212316 VETASSESS

- Technical Director 212317 VETASSESS

- Video Producer 212318 VETASSESS

- Film, Television, Radio and Stage Directors nec 212399 VETASSESS

- Copywriter 212411 VETASSESS

When it comes to accommodation in cities, I tell people to check the real estate sites first for something you can afford, then use Google maps to work out commute times.

-

We could (but probably won't) go into recession today

The Federal Government will be watching closely as the Australian Bureau of Statistics (ABS) releases its gross domestic product (GDP) figures later today.

Last time around, they showed Australia's economy had gone backwards. If that happens for the second quarter in a row, we'll be in a technical recession.

The term, "recession" is this arbitrary thing a lot of us are starting to roll our eyes at.

In a nutshell, China's buying our resources again so we can all breathe.

So we're out of the woods?

Well, no.

The expectation is that annual growth will remain around 2 per cent. According to Trading Economics, the average rate for Australia from 1960 until 2016 was 3.49 per cent.

Many economists think Australia's "potential" growth rate has slowed down, in part because of our aging population, so they see the par annual growth figure being around 2.75-3 per cent to keep unemployment steady

-

Insecure, stressed, and underemployed: The daily reality for millions of Australians

The rise of the part-timer

The sectors of the economy that have enjoyed increased activity are healthcare, hospitality, and tourism. These sectors tend to be biased towards hiring part-time workers.

During the 1980s and 1990s both men and women were working more, and earning more (excluding the recession). Recently, however, the economy's been unable to sustain those jobs.

Now, women tend to be working 25 hours a week, while men also work 25 hours a week (in trend terms). So, overall, the household is working more, but because both jobs may not be strictly full-time, the actual combined take-home pay at the end of the day is less.

So yes, you guessed it, overall we're working more, for less pay.

-

OK, so I'm hoping to round-off this general intro to what's happening in Oz economics with ..

Why are we still buying houses we can't afford?

When will we get to the point that we just say NO?

this has the potential to be like what happened in the US — maybe even worse.

The pros and cons of some of the top suggestions to make buying a house more doable, along with the likelihood of them ever actually happening. "In Sydney, Brisbane and Melbourne it's nothing but a speculative, credit-fuelled housing bubble. It's what happened in Ireland and what happened in a lot of parts of the US in the past decade," he says.

"A lot of people thought the housing market was invincible and it could only go up and one day it crashed and it burned a lot of people, and the financial system along with it."

Youth unemployment in Australia is currently sitting at 13.3 per cent.

-

Well it had to start happening but I didn't think interest rates would start heading north until later on in the year. Wasn't the Reserve Bank, nor the Federal Govt, but the good old banks are taking it upon themselves to do it. One of the major 4 Banks increased home loan rates to existing loans and investment loans. 25 basis points to home loans. JP Morgan advised yesterday that housing investors could expect to see hikes of 3% in the near future. Lot of people gonna get caught out. Once again I hope I'm wrong.

-

I think you will find the articles on this site very interesting and informative:

The articles explain how the central banking system now REALLY works, why interest rates are no longer influenced primarily by a countries central reserve, and why so much of the money supply is tied to mortgages. It is a serious site by real economists and verifiable by Bank of England technical papers.

-

Can you post here short version for lazy guys?

-

Here is a link to some videos they made:

http://positivemoney.org/how-money-works/banking-101-video-course/

There is also one specifically about housing: http://positivemoney.org/issues/house-prices/

The key fact to understand is that because we now have 97% of our money held in electronic accounts (3% is paper & coin) and because BANKS (not the government!) create this electronic money at the point at which they make a loan (very often a home mortgage), the system is prone to problems of price inflation of certain kinds of assets (ie housing and land), instability (a debt is created at the same time as the new money), and the inability of a Countries' central reserve bank to have any real influence on the system (which is why we have seen decades of ever dropping interest rates - even negative (really weird!) rates - with no stimulating impact on the economy.

With housing, we are really in big trouble because (in my opinion) the system makes it likely that houses will continue to strongly inflate in price with occasional big drops like the 2008 sub-prime crash in the USA. (So you will likely loose slowly over time if don't buy a house and you MAY lose really big if you do by a house! )

Personally, I am not a socialist, but I certainly don't support unfettered capitalism either - the system needs to change.

-

Their approach is very popular lately, but had been used for long long time. Idea it so focus on bankers, as if they are some separate evil entity. Such sites and papers have huge flaws, like even not understanding that is the role of government and central banks.

Home prices and mortgages is also nothing new, it is indirect tax that ruling class imposes on workers.

Personally, I am not a socialist, but I certainly don't support unfettered capitalism either - the system needs to change.

Where is no good capitalism variants. So, improving capitalism is waste of time.

-

@Kinvermark thanks for those 2 links, fascinating stuff.

"So you will likely loose slowly over time if don't buy a house and you MAY lose really big if you do by a house!"

That seems to be the situation so many young people are facing. Possibly dammed if they do, and dammed if they don't. Their high levels of debt is just a way of life that they've grown up in, and that's before a lot of them have a mortgage.

-

That seems to be the situation so many young people are facing. Possibly dammed if they do, and dammed if they don't. Their high levels of debt is just a way of life that they've grown up in, and that's before a lot of them have a mortgage.

It is false choice.

If some rapist came and asked you choose one of two ways he want to fuck your daughter you won't be thinking what to choose. Here the solution is the same.

-

@Vitaiy_Kiselev Good point.

-

Improvements are clear

Property Council Australia’s deputy executive director of the Victorian division, Asher Judah, said affordable housing in Melbourne was getting worse every year while also blaming the soaring cost of stamp duty.

He said stamp duty had increased a whopping 795 per cent. Back in 1995, the average home cost $131,000 and stamp duty cost an extra $4000.

But today, people are paying $620,000 for an average home but $32,000 extra for stamp duty.

“On a 25-year mortgage, you’ll pay $24,000 in interest on the stamp duty so basically in total it costs $56,000 per house on average in Victoria over the life of a mortgage.”

-

That link is a very well written and accurate document of the present situation. Stamp duty is one of the biggest hurdles young and older people have to face financially when buying property. They also have big expenses with State government, local councils, and conveyancing , who have money making tools that add exorbitant price on top of actual property value. Rivers of gold for the Banks and Governments in that order. Neither give a fuck about our children and their children.

-

Neither give a fuck about our children and their children.

Well...

Under capitalism a democratic republic, like every other form of state, is nothing but a machine for the suppression of the proletariat. The big bourgeois knows this from his most intimate acquaintance with the real leaders and with the most profound (and therefore frequently the most concealed) springs of every bourgeois state machine.

:-)

Howdy, Stranger!

It looks like you're new here. If you want to get involved, click one of these buttons!

Categories

- Topics List23,990

- Blog5,725

- General and News1,353

- Hacks and Patches1,153

- ↳ Top Settings33

- ↳ Beginners256

- ↳ Archives402

- ↳ Hacks News and Development56

- Cameras2,366

- ↳ Panasonic995

- ↳ Canon118

- ↳ Sony156

- ↳ Nikon96

- ↳ Pentax and Samsung70

- ↳ Olympus and Fujifilm100

- ↳ Compacts and Camcorders300

- ↳ Smartphones for video97

- ↳ Pro Video Cameras191

- ↳ BlackMagic and other raw cameras116

- Skill1,960

- ↳ Business and distribution66

- ↳ Preparation, scripts and legal38

- ↳ Art149

- ↳ Import, Convert, Exporting291

- ↳ Editors191

- ↳ Effects and stunts115

- ↳ Color grading197

- ↳ Sound and Music280

- ↳ Lighting96

- ↳ Software and storage tips266

- Gear5,420

- ↳ Filters, Adapters, Matte boxes344

- ↳ Lenses1,582

- ↳ Follow focus and gears93

- ↳ Sound499

- ↳ Lighting gear314

- ↳ Camera movement230

- ↳ Gimbals and copters302

- ↳ Rigs and related stuff273

- ↳ Power solutions83

- ↳ Monitors and viewfinders340

- ↳ Tripods and fluid heads139

- ↳ Storage286

- ↳ Computers and studio gear560

- ↳ VR and 3D248

- Showcase1,859

- Marketplace2,834

- Offtopic1,320